We recommend the following resources for help in estimating your pension.

Online calculator

This online calculator lets you key in your age, wage, and service information, and quickly estimates your future monthly pension.

Estimate your pension now

Pre-Retirement Orientation online presentation

If you're within three to five years of retirement you may want to view this pre-retirement online presentation. An experienced Michigan Office of Retirement Services representative fully explains the plan and the process.

Your first step in estimating your pension will always be to calculate your final average compensation (FAC). Then you use the pension formula to calculate your straight life pension. Once you know your straight life amount, you have a basis for estimating an early reduced, survivor, and equated pension.

It's very important that you understand the concepts presented here before you make irrevocable selections you'll have to live with throughout your retirement. Once you're familiar with these fundamentals you can move on to the next section for step-by-step help in estimating your pension.

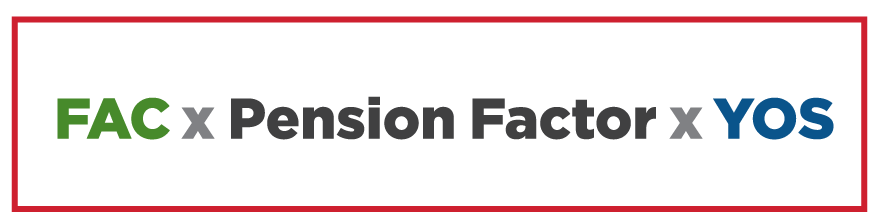

The Pension Formula

Your annual pension is based on a formula that multiplies your FAC under the Defined Benefit (DB) Plan by a pension factor times your years of credited service (YOS) under the DB Plan.

Note: There are different pension formulas for covered employees and conservation officers. See the Covered Employees & Conservation Officers section for more information.

If you're in the DB 30 or DB/DC Blend Plan, your FAC and years of service are determined as of the date you switch to the Defined Contribution (DC) Plan for the purpose of your pension calculation. For members in the DB/DC Blend Plan, that date is March 31, 2012.

Final average compensation (FAC)

Your highest three consecutive years of compensation under the DB Plan are averaged to determine your FAC. If you are a conservation officer, your highest two consecutive years of compensation are used. See details on the types of compensation used in your FAC.

Note: Your highest consecutive years of earnings may have occurred earlier in your career; however, we still refer to it as your FAC.

Pension factor

The pension factor for most state employees is 1.5% (0.015). Conservation officers and covered employees working with prisoners use a different factor and formula.

Years of service (YOS)

Your years of service (YOS) reflect the years, or fractions of years, you have worked for the State of Michigan or one of its noncentral agencies under the DB Plan. You are credited with a full year if you work 2,080 regular hours; however, you may earn no more than 1 YOS credit in any given year.

Only regular, non-overtime hours are counted. Any work that is less than full time or intermittent is evaluated using the regular hours worked converted to a fraction of a year. For example, if you work half time you earn 0.5 YOS for each year of employment. (Exception: You are not considered part time if you work a shortened schedule due to Voluntary Plan A measures, mandatory furlough hours, or the banked leave time program hours. You'll get full credit.)

You may receive service credit for any military leave of absence or workers' compensation leave of absence that occurs during your state employment.

Credited service can also include any additional service credit purchased or transferred. For more information, see Adding to Your Service.

You Have a Choice of Payment Options

The pension formula calculates your straight life pension. All calculations for pension payment options begin by figuring your straight life amount, which is adjusted depending upon which plan or option you are choosing. See details on pension options.

When you begin receiving your pension, any DB pension contributions you paid into the retirement system are paid out first. For more information about this topic, read about your contributions.

Choose your options carefully

You must choose your payment option when you apply for your pension. After your retirement effective date, you will not be able to change your option or your designated survivor pension beneficiary. If you get married after you retire, you may be able to add your spouse to your insurance coverage.