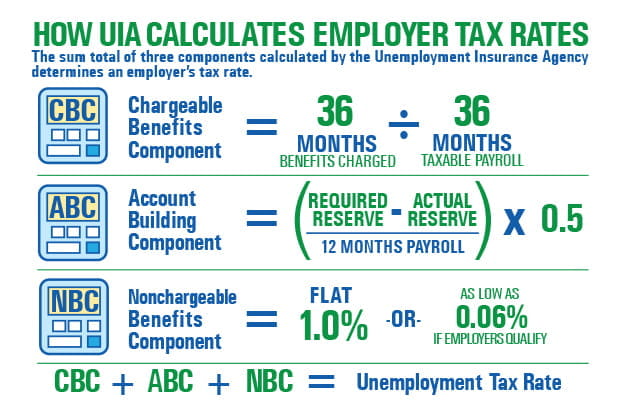

Unemployment Insurance Tax Rate Calculation

We have prepared a sample unemployment insurance tax rate calculation. The sample shows how each of the three components that determines an employer's tax rate is calculated.

Sample Tax Calculation

Form UIA 1771 (Tax Rate Determination for Calendar Year 20__) gives you all the information you will need to calculate your unemployment tax rate. Suppose, for example, your Form UIA 1771 showed the following numbers:

ACTUAL RESERVE: ..............................41,991.80

TOTAL PAYROLL (12 Months): …....2,428,871.34

REQUIRED RESERVE: .........................91,082.68

TAXABLE PAYROLL (36 Months): ...2,972,332.91

BENEFIT CHARGES (36 Months): …....32,869.00

Chargeable Benefits Component:

The calculation is done this way:

36 months of benefit charges / 36 months of taxable payroll = CBC

Taking the sample numbers from above:

32,869.00 / 2,972,332.91 = .0110 = 1.1%

The result is rounded to the next higher 0.1%. (In this example, the fourth decimal place was a "zero," and no rounding was done.)

Account Building Component:

The calculation is done this way:

[(Required Reserve) -(Actual Reserve)] / 12 months of total payroll X 0.5 = ABC

Taking the sample numbers from above:

91,082.68 – 41,991.80 = 49,090.88 ÷ 2,428,871.34 = .02021 X 050 = 0.0101 = 1.10%

If there is any remainder (as there is here with the "1" in the fourth place to the right of the decimal), the result is rounded up to the next higher 0.1%.

Nonchargeable Benefits Component:

This component is generally a flat 1.0% for all contributing employers with three or more years in business. However, for employers with no, or very few, benefit charges the Nonchargeable Benefits Component (NBC) can gradually become as low as 0.06% (6/100).

Unemployment Tax Rate:

For an employer with three or more years of business experience, the unemployment tax rate is computed by adding together the three components:

Chargeable Benefits Component: ................1.1%

Account Building Component .......................1.1%

Nonchargeable Benefits Component: ……...1.0%

UNEMPLOYMENT TAX RATE: ...................3.2%